I decided to do a scatter on this after reading the great analysis Jim Hamilton did on the US Treasury 10 year rally and how this was a "conundrum". While very comfortable with his analysis of risk premium and GDP expectations - at first I was all set to agree - I decided to pull the data. I conclude there is no conundrum but a rare powerful technical move of the curve in anticipation of a sudden Fed Funds hike, a hike that given the pressure building will certainly be well before year end 2014. To my read it is akin to how the bay will empty of sea water prior to the arrival of the tsunami.

http://econbrowser.com/archives/2014/08/bond-market-conundrum-redux

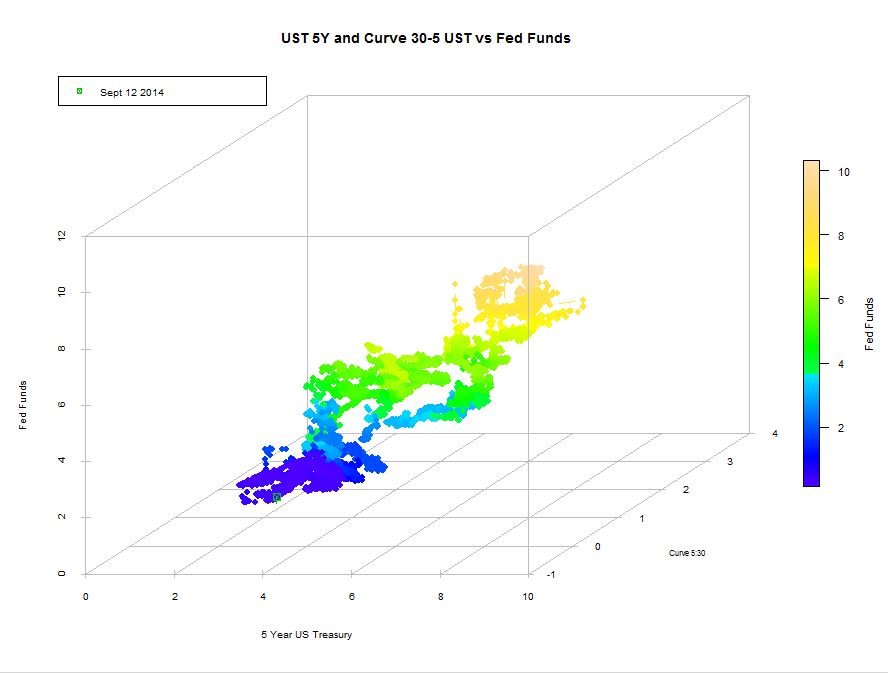

Over the long run the 5:30 curve is an equivalency to the 5 year UST yield with usually a vol ratio (5 year UST YV/32) making a .4 outright 5 y UST to every 1 5y amount in the 5:30.

However that vol ratio is now flipped and is 1.4:1 outright to 5:30.

To me this is indicative of significant if not massive pressure on the curve to realign so as to be priced for a regime shift - since the 5 year is still anchored in ZIRP, it means the longer maturities rally harshly to flatten the curve. Then after the Fed hikes, the curve will continue to flatten but the relationship of 5 y UST now normalized to the curve.

The surge in vol of the 5:30 relative to outright 5 y UST indicates to me a regime jump is about to occur, certainly well before year end. That regime shift would be a surprise rate hike that will lead to a 2 1/2% to 3% 5 year UST imminently.

Note that the small formation under the 8/30/2014 is the worst of the crisis, when it seemed calamity was to occur, from December 08 to January 2009. It is unlikely we reach such a stressed position so I suspect the 5 year (and UST yield in general) jumps suddenly to the prior regime. That is marked by the yellow arrow.

Those who have done well in the flattener to date should swap that position for puts on the 5 y UST.

For open 9/8/2014 followup:

The 5 year UST vs the UST 30s to 5s did move from the above 9/2/2014 opening. The 30s5s backed 6 basis points and 5 year UST backed 19 basis points, for a total net P/L impact, if you did the above swap, of 25 basis points or $8900 per million 5 year UST par amount. So far so good. I think there is a boundary at the data point of 8/29/2014 close.

No comments:

Post a Comment